Determining Beta Values in R

- Frankie Monzon

- Aug 19, 2018

- 1 min read

Updated: Aug 31, 2018

In a recent LinkedIn post, I shared a function for determining beta values.

The R programming language is a very useful tool for analytical work and has been critical to my case studies in business valuation.

As a bit of background, betas are used in discounted cash flow analysis to help determine the cost of equity capital used within that method of business valuation.

In the Capital Asset Pricing Model (CAPM), the cost of equity, Re is defined as the following discount rate, built from a risk free rate (often a government bond rate of the government in which the company in question operates or derives the most significant portion of its revenue), a beta value measuring relative risk (price sensitivity of the asset with respect to measures of the overall market on which it trades, e.g. the S&P 500 for US companies), and the equity risk premium, the rate of return expected on a market-typical equity investment, over and above the risk free rate,

Re = Rf + β (Rm - Rf).

This discount rate, its typical range, and an expected level of precision are key for performing the calculations of discounted cash flow analysis, whereby future cash flows are used to determine a theoretical value for whole companies and their shares.

While beta values may be available from various sources, recently derived values of known precision are typically unavailable to the nonexpert.

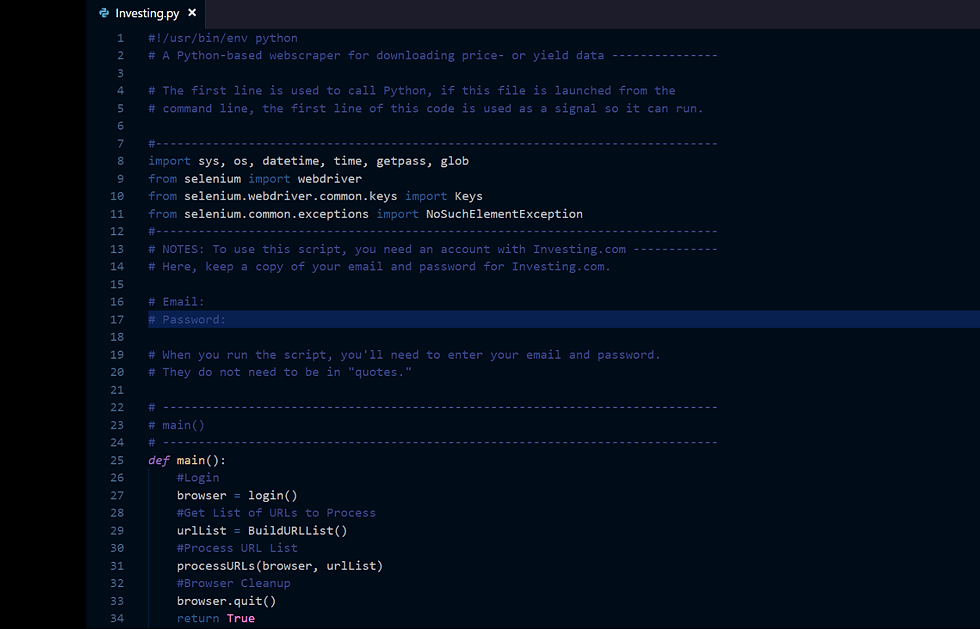

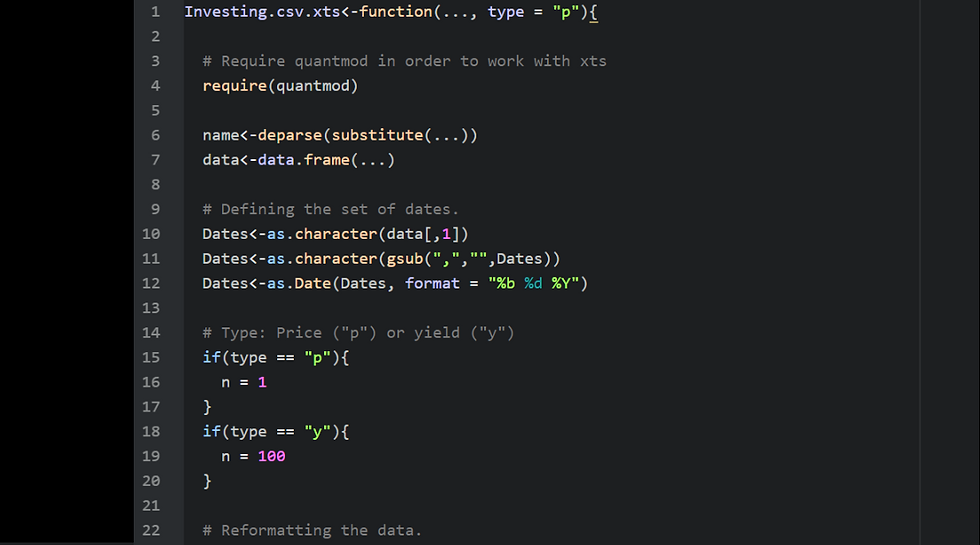

Here you'll find code for the definition of the function!

https://www.linkedin.com/pulse/determining-beta-values-within-r-franklin-monzon/

Comments